Home Loan

Finance up to 90% of the cost and secure your dream home

with easy-to-manage monthly payments.

- Attractive interest rates

- Easy & flexible eligibility norms

- Tenure of up to 30 years

For more information

Please share the details

Reasons to get a Home Loan with HENOX

Flexible Repayment Period

- Flexible Repayment Period

Choose from multiple repayment options you are eligible for such as Step-up, Step-down, and Extended tenure.

Long-term Appreciating Asset

- Long-term Appreciating Asset

Transparent Processing

- Transparent Processing

Tax Benefit

- Tax Benefit

Interest Rates Available*

(Any Amount)

(Upto 50 lakhs)

(Any Amount)

(Upto 50 lakhs)

Who Can Apply For Home Loan?

Find out if you are eligible for applying for a home loan

Self Employed Professional

Self Employed Non-Professional

HOME LOAN AMOUNT

TENURE (1 TO 30 YEARS)

RATE OF INTEREST (7 TO 25%)

CURRENT AGE

MONTHLY INCOME

CURRENT MONTHLY OBLIGATIONS

YOU ARE ELIGIBLE FOR A LOAN OF

₹5,40,000*

FOR A TENURE OF 30 YEARS

EMI @ 9% INTEREST RATE

₹4,339*

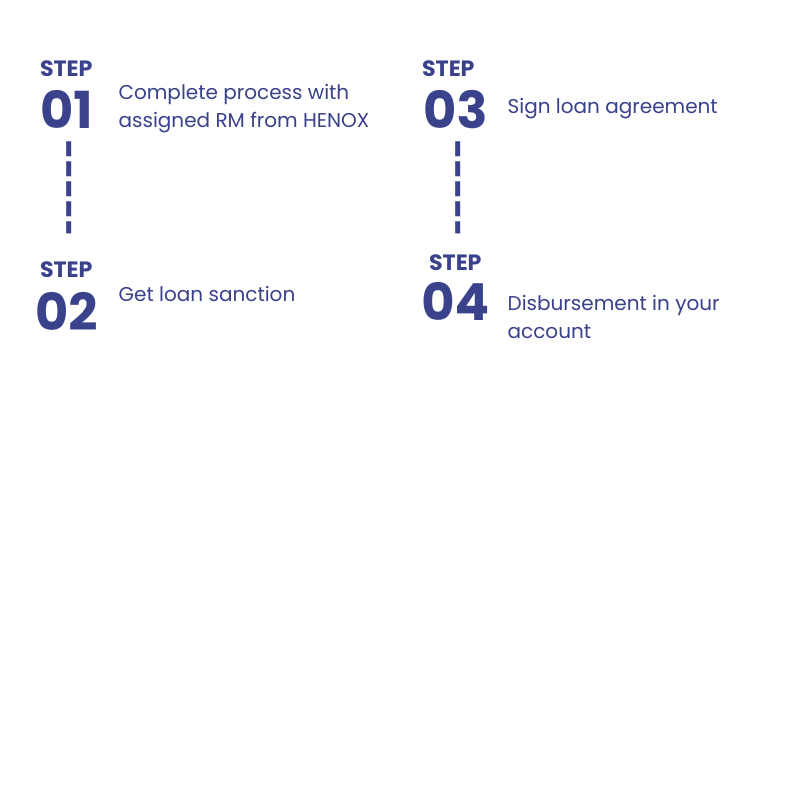

Get A Home Loan In 4 Easy Steps

Home Loan Eligibility

Eligibility criteria

- Nationality | Indian citizen

- Minimum age for applying | 21 years

- Maximum age at loan maturity | 60 years for Salaried & 70 years for Self-employed

- Good credit history | A CIBIL Score of 650 or new to credit

- Employment | Salaried or self-employed

Fees & Charges

PROCESSING FEES

0.25% to 1.50%

CONVERSION CHARGES

STATUTORY AND LEGAL CHARGES

• Stamp Duty

• Legal and other statutory charges

• Insurance Premium

• Creation charge with ROC

• MOE/MOD/Registration

PART PAYMENT/PRE-CLOSURE/FORECLOSURE CHARGES

- other than business purpose – NIL

- Business Purpose – 4 % of principal outstanding and lock-in charges as applicable

- 4% of principal outstanding paid and lock-in charges if any

OTHER CHARGES

Late payment penalty / Non Conformance with any covenants / stipulated conditions

- When facility amount is equal to Rs. 5 lacs or lesser – Rs.50 per loan

- When facility amount is greater than Rs. 5 lacs – Rs.100 per loan

Disclaimer: * – The above charges constitute the rack rate for all customers. Actual charges for any customer, if different, will be as communicated at the time of loan sanction and disbursal and will be subject to changes from time to time.

Documents Needed

Salaried**

- Proof of Identity and Address

- Proof of Income

- Bank statement showing salary

- Proof of Other Income:

Self-Employed**

- Proof of Identity and Address

- Proof of Income

- Bank statement showing salary

- Proof of Other Income:

- Property Documents:

Tax Planning

Save Tax, invest more,

reach goals

- Tax-saving options, one click

- Save tax under different sections

Secured Business Loan

Secure business loans

for you

- Low interest, flexible payments

- One app, quick dispersals

FAQs on Home Loan

ABHFL will determine your home loan eligibility based on your repayment capacity and the value of the property you are purchasing. Your repayment capacity is assessed based on the following factors:

- Income: ABHFL will consider the income of all applicants, as well as any other sources of income, such as rental income or investment income.

- Age: ABHFL will also consider the age of the primary applicant. Borrowers must be at least 21 years old and cannot be older than 70 years old at the time of loan maturity.

- Existing debt obligations:ABHFL will also consider your existing debt obligations, such as EMIs on other loans or credit cards.

- Employment: ABHFL will also consider the stability and continuity of your employment. Borrowers must have a steady income and be able to demonstrate their ability to repay the loan.

Once ABHFL has assessed your repayment capacity, it will determine the maximum loan amount that you are eligible for. The maximum loan amount is typically capped at 90% of the property value.

The following self-attested documents are required for home loan approval:

For Salaried Individuals:

- Proof of identity and address: Passport, voter ID card, driving licence, job card issued by NREGA, Aadhaar card, registration certificate, PAN card (PAN card only as identity proof), or any other document acceptable to ABHFL.

- Proof of income: Latest 3 months salary slip showing all deductions and Form 16.

- Bank statement where salary or income is credited: Latest 6 months.

- Proof of other income: Rental receipts or documents showing receipt of income.

- Property documents: Copy of title documents and approved sanction plan.

For Self-employed / Professional / Partnership / Company:

- Proof of identity and address: Passport, voter ID card, driving licence, Aadhaar card, registration certificate, PAN card (PAN card only as identity proof), or any other document acceptable to ABHFL.

- Proof of income: IT returns or financial documents for the last 2 years and income computation certified by a chartered accountant for the last 2 years.

- Bank statement where income is credited: Latest 6 months.

- Proof of other income: Rental receipts or documents showing receipt of income.

- Property documents: Copy of title documents and approved sanction plan.

ABHFL may request additional documents to process your loan.

You must submit all required documents along with your loan application form.

The maximum tenure for a home loan from ABHFL is 30 years. However, the tenure cannot exceed the borrower’s retirement age or 60 years, whichever is earlier.

Yes, it is mandatory to have a co-applicant for a home loan. This requirement is in place to ensure that there is a second party financially responsible for the loan, which helps to reduce the risk for the lender. If the property is jointly owned, then both parties must be co-applicants. If the property is solely owned, then any member of the immediate family, including spouses, parents, children, or siblings, can be a co-applicant.

Yes, you can get preliminary approval for a home loan before finalising your property purchase. This is known as a PNI (Property Not Identified) Sanction Letter. The PNI Sanction Letter will be based on your income eligibility and will allow you to identify the property you wish to purchase. The final sanction of your home loan will be based on the assessment of the identified property and may be subject to further underwriting. If the property is under construction, please consult with your assigned sales manager to determine its acceptability.

The processing time for home loan applications typically takes 15 working days, provided that all required documents are submitted and the application is complete.

ABHFL calculates home loan interest rates on a monthly, reducing balance basis. The interest rate applied is the prevailing rate of interest (ROI) on your loan, which is linked to our internal floating reference rate, referred to as the ABHFL Reference Rate (ARR).

Yes, an upfront, non-refundable processing fee is required for all home loan applications. The processing fee varies depending on the loan amount and is typically up to 1% of the loan amount plus applicable taxes.