Home Loan Balance Transfer

Maximise your savings with us! Transfer your home loan balance for reduced interest rates and longer repayment tenure.

- Hassle-free loan transfer process

- Access additional funds with a top-up loan

- Enjoy reduced interest rates

- Flexible, extended repayment options

For more information

Please share the details

Streamlined loan transfer process with HENOX

Competitive Interest Rates

- Competitive Interest Rates

Easy Repayment Options

- Easy Repayment Options

Restructure Loan

- Restructure Loan

Top-up Loan

- Top-up Loan

Transparency

- Transparency

Which Loans Are Eligible For a Balance Transfer?

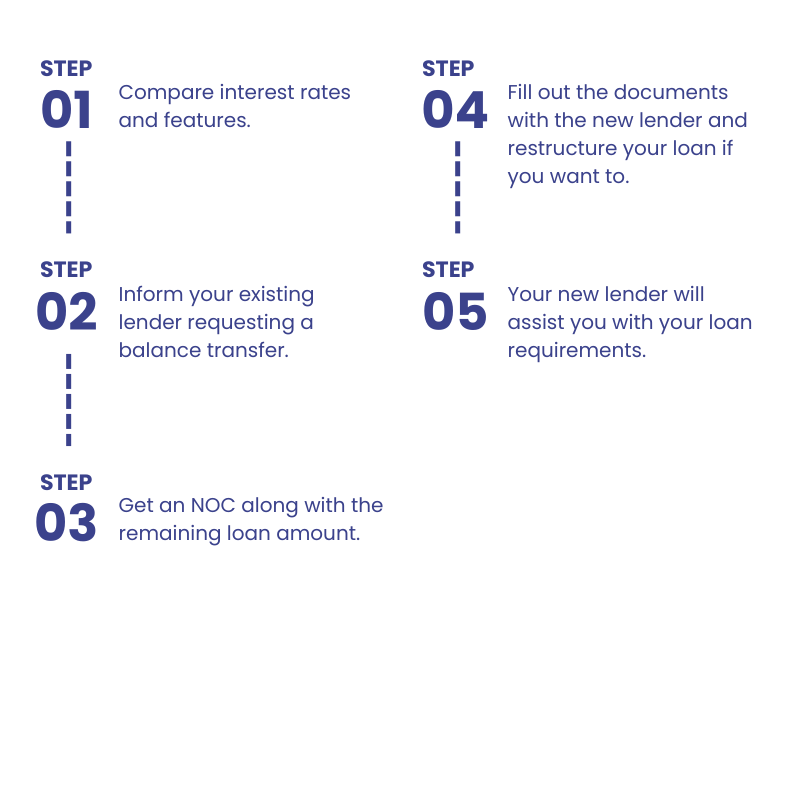

Get A Home Loan In 5 Easy Steps

Interest Rates Available*

Balance Transfer Eligibility

Eligibility criteria

- Nationality | Indian citizen

- Minimum age for applying | 21 years

- Maximum age at loan maturity | 60 years for Salaried & 70 years for Self-employed

- Good credit history | A CIBIL Score of 650 or new to credit

- Income | Varied criteria depending upon the loan amount. Existing EMIs will also be accounted for.

Fees & Charges

PROCESSING FEES & CHARGES

- Home Loans : Up-To 1% Of The Loan Amount

- Other Loans : Up-To 2% Of The Loan Amount

- Floating rate loans given to individuals, where all applicants and co-applicants are individuals: Nil

- Home Loans (other than floating rate Home Loans to individuals): 2% of principal outstanding

CONVERSION FEE

- When the facility amount is equal to ₹5 Lakh or lesser – ₹50 per property.

- When the facility amount is greater than ₹5 Lakh – ₹100 per property.

STATUTORY AND LEGAL CHARGES

MISCELLANEOUS RECEIPT

- ₹50/- per instance for Consumer and

- ₹500/- for Commercial CIBIL

Documents Needed

Salaried**

- Proof of Identity and Address

- Proof of Income

- Bank statement showing salary

- Proof of Other Income:

- Property Documents:

Self-Employed**

- Proof of Identity and Address

- Proof of Income

- Bank statement showing salary

- Proof of Other Income:

- Property Documents:

Balance Transfer Calculator

Find out how much you can save by transferring your home loan to HENOX!

What is it?

This calculator helps you understand how much you can save by transferring your existing home loan. It compares the total amount you'll end up paying with your current lender to the total you'll pay with HENOX.

How it works?

Simply provide the basic details of your current loan such as the loan balance, your current interest rate, and the repayment tenure, along with the interest rate expected from HENOX, and your desired repayment tenure.

New Eligible Loan Amount

₹ 0

Total Interest

₹ 1000083

Total Payable Amount

₹ 1000083

Amount Saved with BT

₹ 0

Top Up Eligible

₹ 0

Tax Planning

Secure business

loans for you

- Low interest, flexible payments

- One source, quick dispersals

Secured Business Loan

Guaranteed returns with

Fixed Deposit

- Flexible deposit tenures

- ₹5 lakh deposits insured by DICGC

FAQs on Home Loan Balance Transfer

Features:

- Transfer your existing home loan to a new lender.

- Potentially get a lower interest rate, which can save you money on your monthly payments.

- Possibility to extend the repayment term of your loan, lowering your monthly payments.

- Some lenders offer flexible repayment options.

- Possibility to find a lender with better customer service.

Benefits:

- Lower interest rates.

- Extended repayment terms.

- More flexible repayment options.

- Improved customer service.

Here are the steps to apply for a Home Loan Transfer at Henox CAPITAL & FINSERV PVT. LTD. :

1. Check your eligibility: Before applying for a home loan transfer, ensure you meet the eligibility criteria. This typically includes having a good credit history, a stable income, and a decent repayment track record for your existing home loan.

2. Gather the required documents: Prepare the necessary documents for your home loan transfer application. These typically include identity proof, address proof, income proof, property documents, and details of your existing home loan.

3. Choose the desired loan transfer amount: Determine the loan amount you want to transfer to ABHFL. This should be within the transferable limit set by your current lender.

4. Understand the loan transfer terms: Thoroughly read and understand the terms and conditions including the fine print of the home loan transfer agreement offered by ABHFL. Consider factors like processing fees, prepayment penalties, and any applicable discounts.

5. Submit the loan transfer application: Fill out the home loan transfer application form accurately and provide the required documents to ABHFL. You can apply online or by visiting a branch.

6. Undergo credit checks and property valuation: ABHFL will conduct a credit check to assess your creditworthiness and may also evaluate the property to determine its current market value.

7. Receive loan transfer approval and disbursal: Upon approval, you will receive a loan sanction letter outlining the loan terms and conditions. The loan amount will be transferred directly to your existing home loan account, closing that loan and establishing a new one with HENOX.

For any assistance, you can also write to us at Info@henoxcapital.com or call the HENOX customer care number (1800 270 7000).

Yes, ABHFL offers home loan balance transfers, which allow you to transfer your existing home loan from another lender to ABHFL. This can be beneficial if you are seeking a lower interest rate, more flexible repayment options, or access to additional financing. To apply for a home loan balance transfer, simply select the “refinance” option on the application form. You may also be eligible for an additional top-up loan.

Here are some tips to ensure a smooth and hassle-free balance transfer process:

- Start planning early. The earlier you start planning your balance transfer, the smoother the process will be. This will give you enough time to compare the offerings of different lenders and choose the best one for your needs.

- Gather all the required documents. Before you apply for a balance transfer loan, make sure that you have all the required documents in hand. This will help to expedite the processing of your application.

- Keep your lender updated. Keep your lender updated on your progress throughout the balance transfer process. This will help to avoid any delays or complications.

- Be patient. The balance transfer process can take some time, so it is important to be patient. However, if you follow the tips above, you can help to ensure that the process is as smooth and hassle-free as possible.

Here are some things that you should avoid doing when transferring your home loan:

- Don’t rush into a decision. Take your time to compare the offerings of different lenders and choose the best one for your needs. Don’t feel pressured to sign a loan agreement with the first lender that you talk to.

- Don’t forget to read the fine print. Before you sign a loan agreement, be sure to read the fine print carefully. This will help you to understand all of the terms and conditions of the loan.

- Don’t forget to factor in the costs. There may be some costs associated with transferring your home loan, such as processing fees and legal fees. Be sure to factor these costs into your decision.

- Don’t forget to inform your existing lender. Once you have decided to transfer your home loan, be sure to inform your existing lender. They will need to release the title to your home to the new lender.

Pros of a balance transfer:

- Lower interest rate: You may be able to get a lower interest rate on your balance transfer loan, which can save you money on your monthly payments and overall interest costs.

- Better terms: Some lenders may offer better terms on balance transfer loans, such as a longer repayment period, lower processing fees, or waivers on certain charges.

- Top-up loan: You may be able to get a top-up loan with your balance transfer loan, which can help you finance home improvement or other expenses.

Cons of a balance transfer:

- Fees: There may be fees associated with a balance transfer, such as processing fees, documentation charges, and stamp duty charges.

- Prepayment penalty: If you have a prepayment penalty on your existing home loan, you may have to pay it when you transfer your loan.

- Risk of rejection: There is a risk that your balance transfer loan application could be rejected. This could happen if you do not meet the lender’s eligibility criteria or if you have a poor credit score.

There are no direct tax implications of a home loan balance transfer. However, the interest that you pay on your home loan is tax deductible under Section 24(b) of the Income Tax Act, 1961. This means that you can deduct the interest that you pay on your home loan from your taxable income, which can reduce your tax liability. The maximum amount of interest that you can claim as a tax deduction is ₹ 2 lakhs per financial year.

Whether or not you have to pay a prepayment penalty to your existing lender depends on the terms of your existing loan agreement. Some lenders charge a prepayment penalty of up to 2% of the outstanding loan balance. Others may charge a flat fee. If you are considering transferring your loan, be sure to check with your existing lender to see if there is a prepayment penalty and how much it is.

Here are some tips to improve your chances of getting approved for a balance transfer loan:

- Maintain a good credit score. A good credit score shows lenders that you are a responsible borrower and that you are less likely to default on your loan.

- Have a low debt-to-income ratio. Your debt-to-income ratio is the percentage of your monthly income that goes towards paying your debt. A low debt-to-income ratio shows lenders that you have enough income to cover your monthly loan payments.

- Have a stable job and income. Lenders want to see that you have a stable job and income so that you can afford to make your monthly loan payments.

- Have a down payment. A down payment is a percentage of the purchase price of the property that you pay upfront. Having a down payment shows lenders that you are serious about the loan and that you are less likely to default.