Home Loan Top Up

Get a quick, hassle-free loan on your existing home loan.

Attractive interest rates and no restriction on usage.

- Affordable interest rates

- Easy application process

- Borrow up to 80% of property value

For more information

Please share the details

Reasons to buy Top-up Home Loan with with HENOX

Flexibility in usage

- Flexibility in usage

Competitive interest rates

- Competitive interest rates

Customised repayment terms

- Customised repayment terms

Quick processing times

- Quick processing times

Dedicated customer service

- Dedicated customer service

Debt consolidation

- Debt consolidation

Which Loans Are Eligible For a Balance Transfer?

Which Loans Are Eligible For Top-up

Self Employed Professional

Self Employed Non-Professional

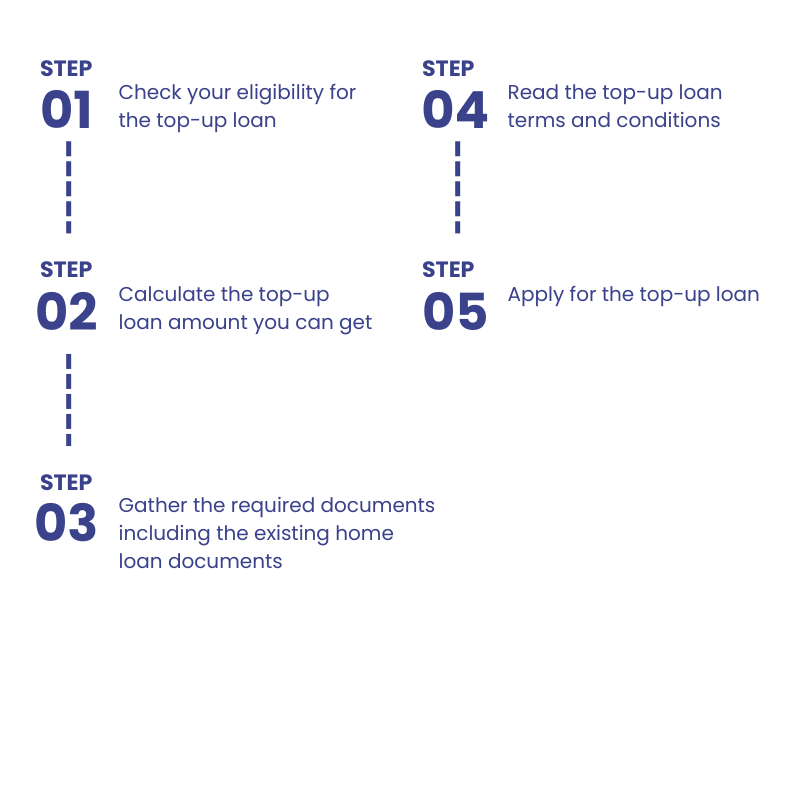

Get A Top UP Home Loan In 5 Easy Steps

Top Up Home Loan Eligibility

Eligibility criteria

- Nationality | Indian citizen

- Minimum age for applying | 21 years

- Maximum age at loan maturity | 60 years for Salaried & 70 years for Self-employed

- Good credit history | A CIBIL Score of 650 or new to credit

- Employment | Salaried or self-employed

Fees & Charges

PROCESSING FEES

CONVERSION CHARGES

STATUTORY AND LEGAL CHARGES

• Stamp Duty

• Legal and other statutory charges

• Insurance Premium

• Creation charge with ROC

• MOE/MOD/Registration

PART PAYMENT/PRE-CLOSURE/FORECLOSURE CHARGES

- Part Payment / Pre-closure is allowed after 12 months from final loan disbursement date

- In case of Part Payment / Pre-closure before 12 months from final loan disbursement date, lock-in period interest will be applicable

- other than business purpose – NIL

- Business Purpose – 4 % of principal outstanding and lock-in charges as applicable.

- 4% of principal outstanding paid and lock-in charges if any.

- Pre-closure statement charges

- Original document retrieval charges

OTHER CHARGES

Late payment penalty / Non Conformance with any covenants / stipulated conditions

- When facility amount is equal to Rs. 5 lacs or lesser – Rs.50 per loan

- When facility amount is greater than Rs. 5 lacs – Rs.100 per loan

Disclaimer: * – The above charges constitute the rack rate for all customers. Actual charges for any customer, if different, will be as communicated at the time of loan sanction and disbursal and will be subject to changes from time to time.

Documents Needed

Salaried**

- Proof of Identity and Address

- Proof of Income

- Bank statement showing salary

- Proof of Other Income:

- Property Documents:

Self-Employed**

- Proof of Identity and Address

- Proof of Income

- Bank statement showing salary

- Proof of Other Income:

- Property Documents:

Disclaimer: HENOX reserves the rights to call upon additional documents at its discretion. The documents will be collected by HENOX.

Tax Planning

Save Tax, invest more,

reach goals

- Tax-saving options, one click

- Save tax under different sections

Secured Business Loan

Secure business loans

for you

- Low interest, flexible payments

- One app, quick dispersals

FAQs on Home Loan

A top-up home loan is an additional loan that can be availed of over and above an existing home loan. It is typically taken by borrowers who have seen an increase in their income, a decrease in their outstanding balance on their existing home loan, or who have additional anticipated expenses. If the borrower wishes to increase the loan amount and take a cash out, they can do so by applying for a top-up loan.

Yes, you can apply for a top-up home loan even if you have refinanced your home loan with ABHFL. The eligible loan amount will be determined based on your current home loan eligibility, which is assessed using the following factors:

- Income of all applicants

- Age of the primary applicant

- Existing income or EMIs

- Stability and continuity of the primary applicant’s occupation

To ensure your eligibility for a top-up home loan, it is recommended to consult with an ABHFL representative to discuss your specific circumstances.

To be eligible for a top-up home loan, you must generally meet the following criteria:

• Existing home loan with ABHFL: You must hold an existing home loan with ABHFL to qualify for a top-up home loan. This ensures that the lender has a comprehensive understanding of your financial situation and repayment capacity.

• Good credit history: A strong credit history demonstrates your ability to manage debt responsibly and makes you a less risky borrower for the lender. A good credit score typically ranges from 700 to 850.

• Steady income: A stable and consistent income stream is crucial for ensuring that you can make the monthly repayments on your top-up home loan. This ensures that your loan is not unduly burdensome on your finances.

• Sufficient property value: The value of your property acts as collateral for the top-up home loan. The lender will evaluate the market value of your property to assess its ability to support the additional loan amount. The top-up loan amount is typically capped at 70–80% of the property’s value.

• Loan-to-Value (LTV): LTV represents the ratio of your outstanding home loan amount to the property’s market value. A lower LTV indicates a higher equity portion, which may be favourable for top-up loan approval.

Top-up home loans typically offer lower interest rates and longer repayment terms than personal loans. This is because the lender has more security as the loan is secured against your property. Also, lower interest rates translate to lower monthly repayments, making the loan more manageable for you. Additionally, top-up loans are secured by your home, which means that you may qualify for a higher loan amount than you would with a personal loan.

The interest rate for a top-up home loan is typically determined based on several factors, including:

- Existing home loan interest rate: The interest rate on your existing home loan often serves as the base rate for the top-up loan. This ensures consistency in your overall interest rate and simplifies the repayment process.

- Credit history: Your credit history plays a significant role in determining the interest rate offered for your top-up loan. A strong credit history, typically reflected by a high credit score, indicates a lower risk to the lender and can lead to a lower interest rate. Conversely, a poor credit history may result in a higher interest rate.

- Loan-to-Value ratio (LTV): The LTV represents the ratio of your outstanding home loan balance to the current market value of your property. A lower LTV indicates that you have more equity in your property, making it less risky for the lender and potentially leading to a lower interest rate.

- Loan amount: The amount of the top-up loan you are applying for may also influence the interest rate. Larger loan amounts may attract slightly higher interest rates, while smaller top-ups may receive lower interest rates.

- Lender’s interest rates: Different lenders have their own internal policies and risk assessment models, which can affect the interest rates they offer for top-up home loans. It is important to compare interest rates from multiple lenders to find the most competitive terms.

- Market conditions: Overall market conditions, such as prevailing interest rates and economic trends, can also influence the interest rates offered for top-up home loans. Interest rates may fluctuate over time, so it is advisable to check current rates before applying for a top-up loan.

In conclusion, the interest rate for a top-up home loan is typically the same as the interest rate on your existing home loan. However, it may be slightly higher, depending on your credit history and other factors.